Margin Call Gets the Most Honest Line in Financial Cinema

Most financial crisis films are interested in the aftermath. The job losses, the foreclosures, the political fallout. Margin Call is interested in the eighteen hours before any of that happens, and that choice turns out to be far more revealing.

The movie takes place almost entirely within a fictional investment bank during one night in 2008, when a junior risk analyst uncovers that the firm's mortgage-backed investments have become so unstable that a single bad day in the market could wipe out the entire company's market value. What follows is not a story of greed in the ordinary sense. This is a story about a room full of smart, well-paid people who calmly and knowledgeably decide to blow up the larger market in order to save themselves from the blast.

The most important scene in the film is not the dramatic boardroom confrontation or the dawn trading sequence. It is a quieter moment earlier in the night, when the CEO, played by Jeremy Irons, asks a junior analyst to explain the risk model to him "in plain English, as if you were speaking to a child." He is not asking because he is stupid. He is asking because the structure of his institution has insulated him from needing to understand it. He runs a firm whose core product he cannot, without assistance, describe. That single detail captures something about large financial institutions that most commentary on 2008 misses entirely.

The crisis was not primarily caused by people who understood the risks and took them anyway. It was largely because of an organisational structure in which the people taking the risks and the people bearing the consequences were effectively different. Traders posting returns on complex instruments were paid for short-term performance. Shareholders, creditors, counterparties and finally taxpayers felt the long term pain. The incentives and the consequences had been surgically divided and no one had good reason to put them back together again.

That's what the film's central decision captures so well. The ethical problem is laid bare when senior leadership decides they have to liquidate their entire toxic position the next morning, throwing it on the market before anyone else realizes what is happening. They know they are passing their losses onto counterparties. They know that those counterparties will be hurt. But they do it anyway, because the alternative is the firm's insolvency. One character says, "We will never be able to trade with those counterparties again." Someone else replies that they probably wouldn't want to anyway, given what's coming. That exchange is the economic thesis of the film in two lines. Reputation is the mechanism that prevents this sort of behavior in a working market. When participants believe a crisis is large enough, they rationally defect, because the reputational cost of defecting in a market that no longer exists is zero.

The 2008 crisis was full of these calculations. Banks stopped lending to each other not because they were being irrational but because the rational response to uncertainty about counterparty solvency is to stop lending. The interbank market froze because trust, which is the actual infrastructure of short-term credit markets, had been quietly hollowed out over years by the accumulation of positions that nobody fully understood. The film's fictional firm is simply the first one to look clearly at the situation and act on what it sees.

There is one line in the film that has always struck me as the most economically honest thing in financial cinema. A senior trader, describing what he and his colleagues do for a living, says they are simply moving money from one place to another, taking a percentage for the movement, and that this is not, in any meaningful sense, wrong. He is not defending it. He is just describing it accurately. The film has the integrity not to contradict him.

The lesson Margin Call offers is not that Wall Street is populated by villains. It is that the system produced rational behaviour at every level, and the aggregate of that rational behaviour was catastrophic. Individual decisions that made sense given each actor's incentives, information, and constraints added up to collective destruction. That is a harder conclusion than simple greed, which is probably why it gets told less often.

More Opinion

Other Columns

Jul 6, 2026

We Read Freakonomics Wrong, and So Did Everyone Else

Freakonomics taught a generation that a clever enough economist could pull hidden truths out of any dataset. The book was not a fraud. The problem is subtler, and more interesting, because it is about what happens to an idea when you make it beautiful.

Jun 28, 2026

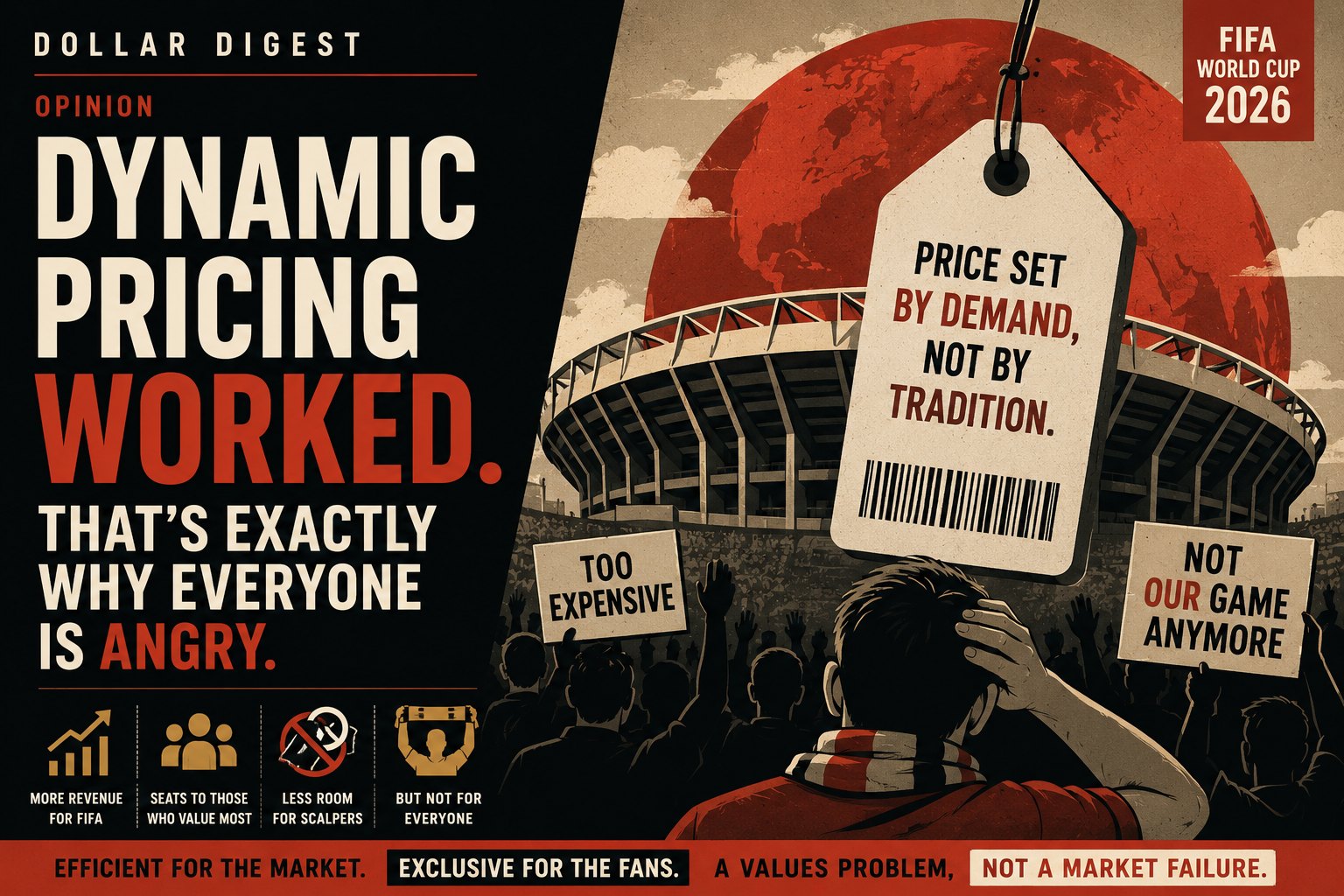

Dynamic Pricing Worked. That's Exactly Why Everyone Is Angry.

The 2026 World Cup sold out almost every seat in almost every stadium. FIFA called it a triumph. Fans called it a rip-off. Both are looking at the same number and reaching opposite conclusions, because they are arguing about two completely different things.

Jun 24, 2026

Chicago Did the Math. Everyone Else Threw a Party.

Sixteen cities looked at the same numbers and said yes. One looked at them and said no. Chicago walked away from the 2026 World Cup, and the economic record suggests it made the only intelligent decision in the entire tournament.

Jun 11, 2026

The Big Short Got the Villain Wrong

Most people come away from The Big Short with the same reading: Wall Street was greedy, regulators were asleep, and a handful of contrarians got rich by being the only ones willing to look at the data. That reading is not wrong. It is just not the film's most important argument.