The Big Short Got the Villain Wrong

Most people come away from The Big Short with the same reading: Wall Street was greedy, regulators were asleep, and a handful of contrarians got rich by being the only ones willing to look at the data. That reading is not wrong. It is just not the film's most important argument.

The deeper claim The Big Short makes, and the one that has aged far better, is about incentive structures rather than individual character. The bankers packaging fraudulent mortgage bonds were not uniquely villainous people. They were people operating rationally inside a system that rewarded them for not looking too closely. Rating agencies gave AAA ratings to bonds built on subprime loans because their fees came from the banks issuing those bonds. Traders sold products they did not understand because their bonuses depended on volume, not accuracy. No single person needed to be corrupt for the entire architecture to become fraudulent. The system did that on its own.

Burry understood this, and it cost him. In 2005, he read through mortgage bond prospectuses that nobody else on Wall Street had bothered to open, identified that the underlying loans were resetting to rates borrowers could not pay, and constructed credit default swaps against the housing market. The banks sold them to him happily, certain he was wrong. His own investors were less relaxed about it. As premiums mounted and the trade sat underwater for months, they demanded redemptions. Burry locked them in, halting withdrawals and weathering a direct confrontation from one of his largest investors. He developed a bleeding ulcer. The trade eventually returned 489% for Scion Capital. Most of his investors never thanked him. The fund closed without ceremony.

That arc is the film's most instructive passage, not because Burry was vindicated, but because of what his vindication required. He had to be willing to lose his professional reputation, his investor relationships, and possibly his fund in order to act on information sitting in publicly available documents. The barrier to seeing the crisis was not access to data. It was that nobody with institutional standing had any incentive to look at it honestly.

This brings the film's closing scenes into focus as one of its most damning conclusions. Eight million people lost their jobs. Six million people lost their homes. Only one banker went to jail. All the while, the institutions responsible for causing this mess were rescued by public funds and rewarded with bonuses. Then, finally, in the closing title card, the film almost offhandedly states that by 2015, several large banks had started selling billions in something called a "bespoke tranche opportunity," which, according to the Wall Street Journal, is just another name for a CDO.

That is not an ironic postscript. It is the thesis. The structural conditions that produced 2008 were not dismantled. They were temporarily embarrassed and then quietly reassembled with new terminology. The incentives that made collective blindness rational were still in place. The people who were wrong paid no meaningful price. The people who were right paid a significant personal one and then closed their funds.

In late 2025, Burry closed Scion Asset Management for the second time. In his letter to investors, he wrote that his estimation of value in securities "is not now, and has not been for some time, in sync with the markets." He posted a photograph of Christian Bale's character lying on the floor surrounded by papers with the caption: "Me then, me now." He has spent years warning that AI valuations reflect the same structure of incentivised blindness that characterised 2005 mortgage markets. He may be wrong. He was also wrong for two years before he was spectacularly right.

The bespoke tranche opportunity is still out there. It just has a different name again.

More Opinion

Other Columns

Jul 6, 2026

We Read Freakonomics Wrong, and So Did Everyone Else

Freakonomics taught a generation that a clever enough economist could pull hidden truths out of any dataset. The book was not a fraud. The problem is subtler, and more interesting, because it is about what happens to an idea when you make it beautiful.

Jun 28, 2026

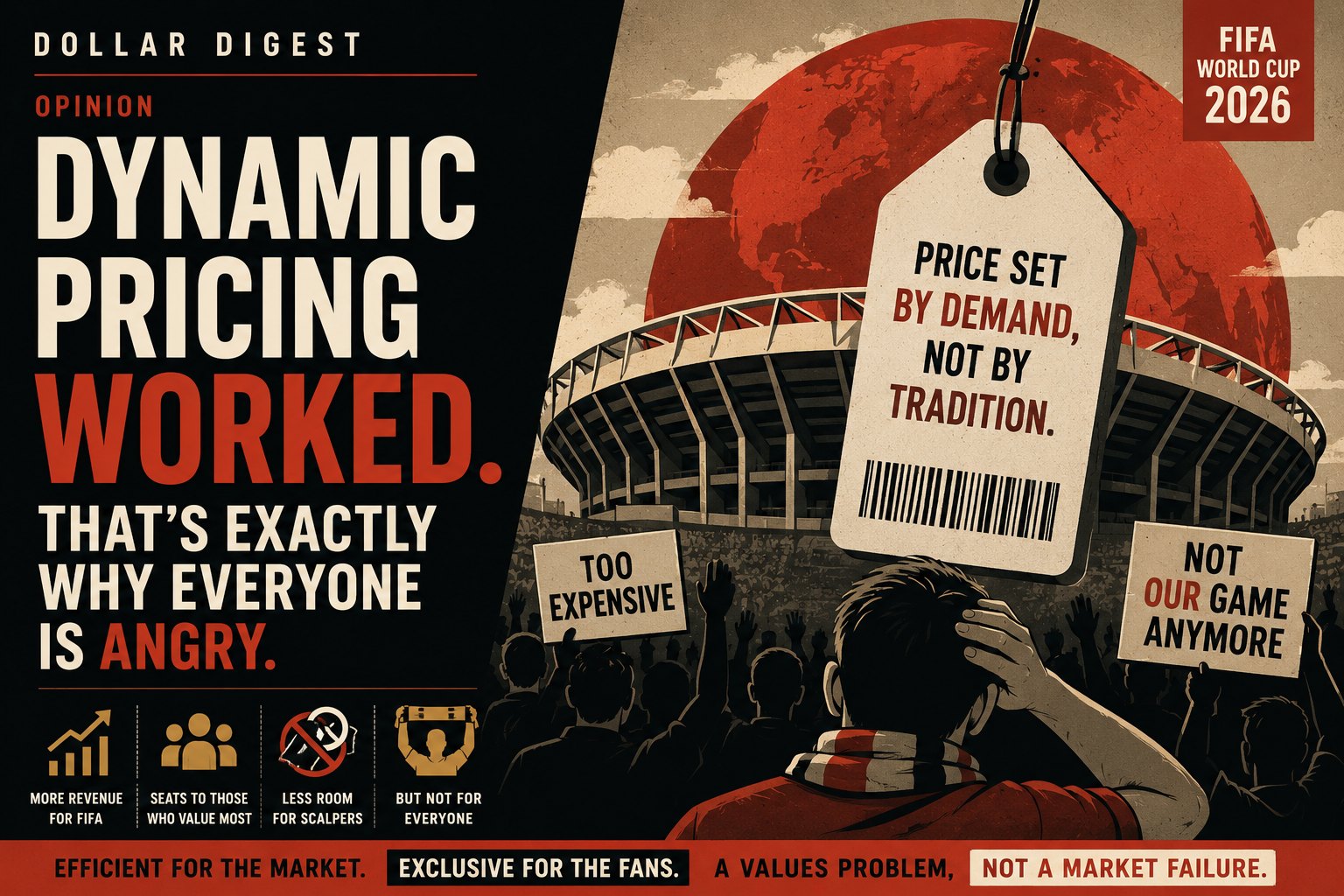

Dynamic Pricing Worked. That's Exactly Why Everyone Is Angry.

The 2026 World Cup sold out almost every seat in almost every stadium. FIFA called it a triumph. Fans called it a rip-off. Both are looking at the same number and reaching opposite conclusions, because they are arguing about two completely different things.

Jun 24, 2026

Chicago Did the Math. Everyone Else Threw a Party.

Sixteen cities looked at the same numbers and said yes. One looked at them and said no. Chicago walked away from the 2026 World Cup, and the economic record suggests it made the only intelligent decision in the entire tournament.

Jun 17, 2026

Margin Call Gets the Most Honest Line in Financial Cinema

Most financial crisis films are interested in the aftermath. The job losses, the foreclosures, the political fallout. Margin Call is interested in the eighteen hours before any of that happens, and that choice turns out to be far more revealing.