Housing has become the defining economic frustration for young people. Home prices continue to rise faster than incomes, rents consume growing shares of household budgets, and governments across the world are promising to build more homes. Yet despite years of housing initiatives, affordability remains elusive.

This article argues that the housing crisis is no longer primarily a construction problem. It is increasingly a demographic problem that many governments failed to anticipate. Without accounting for the forces driving housing demand, building more homes alone is unlikely to restore affordability. Without addressing the underlying demographic forces driving demand, building more homes alone is unlikely to restore affordability.

The traditional explanation for rising housing costs is straightforward: there are not enough homes. This is so in many countries. The United Kingdom has chronically underbuilt compared to experts' estimates of need. Canada's housing agency estimates the country needs millions of additional homes by 2030 to restore affordability. But looking only at supply misses a more important question: why has demand been so strong in the first place? The answer starts with demographics.

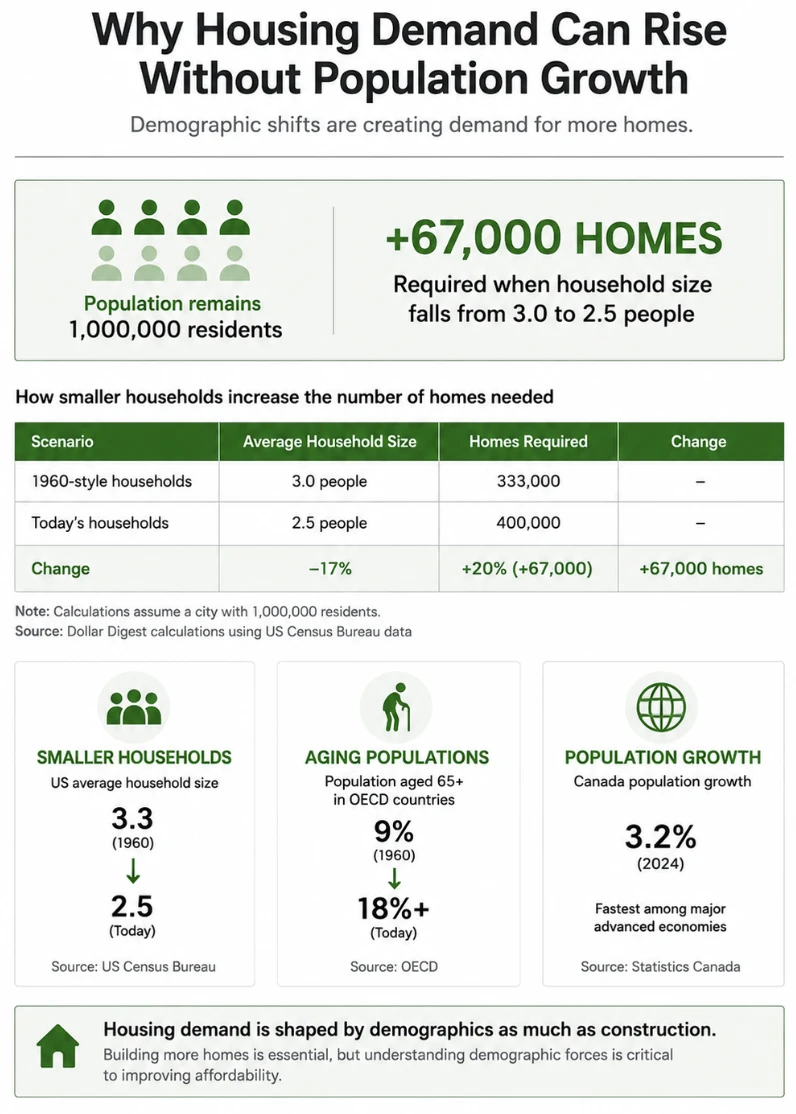

Over the past several decades, households have become smaller across much of the developed world. In the United States, the average household size has fallen from around 3.3 people in 1960 to roughly 2.5 today (US Census Bureau). Similar trends exist across Europe and parts of Asia. Even when population growth slows, smaller households mean more housing units are required to accommodate the same number of people.

This creates a hidden source of housing demand. A city of one million residents living in households of three people requires roughly 333,000 homes. If average household size falls to 2.5 people, that same city suddenly needs 400,000 homes. No population growth is required. Demand increases simply because people live differently.

Aging populations add even more pressure. Across OECD countries, the share of people aged 65 and above has risen from 9% in 1960 to more than 18% today (OECD). Older homeowners often remain in family-sized homes for longer, reducing turnover in the housing market. At the same time, younger generations are entering the market later due to affordability challenges, creating bottlenecks across multiple age groups.

In some countries immigration has added to these pressures. Canada's population grew by roughly 3.2% in 2024, one of the fastest rates among advanced economies, and housing construction struggled to keep pace (Statistics Canada). The result was predictable: housing construction could not keep pace with population growth, causing affordability to deteriorate even as governments increased housing targets.

The key takeaway is that demographics are becoming more and more the driver of housing affordability, not just construction. Governments can accelerate approval of building and promote development but those policies will have limited impact if they do not take into account smaller households, aging populations and migration trends.

This is important because much housing policy is aimed at symptoms, not causes. We need to build more homes, but that is not the whole solution. The countries most likely to improve affordability will be those that align housing policy with demographic reality rather than treating housing shortages as purely a construction challenge.

The real test is whether governments can move beyond short-term housing targets and begin planning for the demographic shifts that will shape demand over the next two decades. If household sizes continue shrinking and populations continue aging, can housing ever become affordable again without a fundamental rethink of how cities are planned?